Last week, the global economy sent multiple warning signals simultaneously, including the U.S.-China summit ending with smiles but no substantive outcomes; the world's bond markets experiencing their most severe sell-offs in years; the Fed meeting minutes hinting at interest rate hikes; and the prolonged Middle East war exceeding market expectations. Domestically, there was good news with stronger-than-expected Q1 GDP and a major challenge ahead regarding the 400 billion baht stimulus package.

The Trump-Xi Jinping summit in Beijing ended with a friendly atmosphere. Trump called Xi a “great leader.” China proposed a new framework for relations under the concept of “Constructive Strategic Stability.” Signs of trade progress included orders for 200 Boeing aircraft, increased agricultural and energy imports, and plans to establish joint trade and investment committees.

However, markets responded negatively due to the absence of key agreements on rare earth minerals or artificial intelligence. Taiwan tensions remained high. Overall, INVX assessed the summit as a “Tactical De-escalation, Not Strategic Resolution,” meaning it eased short-term tensions but did not resolve the long-term structural competition among superpowers. The advanced technology war continues.

Global bond markets faced the most intense simultaneous sell-off in years. The main drivers were U.S. consumer inflation in April rising to 3.8% and producer prices accelerating at the fastest pace since 2022. This pushed U.S. 10-year Treasury yields up to 4.59%, UK 30-year Gilts to 5.86%—the highest since 1998—and Japanese 30-year government bonds to a record 4.085%. The surge in Japanese bond yields raises risks of a Yen Carry Trade unwind, potentially causing global liquidity tightening.

More concerning was the latest Fed meeting minutes revealing that most Fed officials are signaling readiness to raise interest rates if inflation remains persistently above the 2% target. Many members even proposed removing language suggesting a tilt toward rate cuts, opening the door for hikes if needed. This marks a major shift from earlier in the year when the Fed signaled easing. The root cause remains the Middle East war, with oil prices holding above $110 per barrel, keeping supply chains and energy costs high, thereby prolonging inflationary pressures.

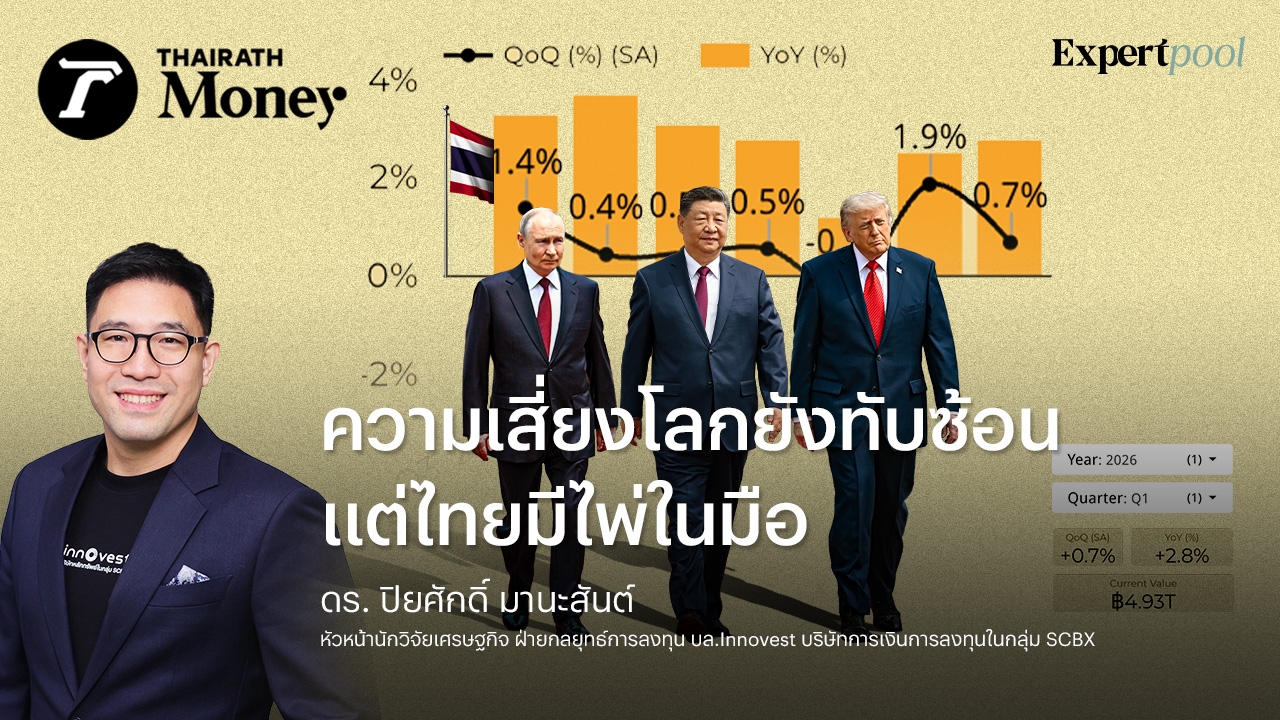

In Thailand’s bond market, the 10-year yield rose to 2.41%, pressured further by the 400 billion baht borrowing decree that will push total borrowing in fiscal 2023 beyond the peak seen during COVID-19. INVX maintains year-end forecasts of 4.40% for the U.S. 10-year Treasury and 2.50% for Thailand’s 10-year bond, higher than median market analyst estimates. They recommend closely monitoring developments, especially regarding the war's impact on energy prices and inflation.

Good news this week came from Thailand’s Q1 2023 GDP, which grew 2.8% year-on-year—above the market’s 2.2% forecast and close to INVX’s 3.0% estimate—up from 2.5% in the previous quarter. The main drivers were private investment surging 10.1%, the highest in 14 quarters, led by digital and electronics industries, along with strong export growth of 15.1%. However, heavy imports caused the trade balance and net exports (exports minus imports) to be negative, weighing on the economy.

However, part of the strong figures stemmed from front-loading of exports and imports ahead of clearer impacts from the Middle East war. This momentum is expected to slow in Q2-Q3 as high energy costs begin to feed through into higher living and business costs.

The National Economic and Social Development Council maintains its 2023 GDP forecast at 2.0%. INVX has revised its upside GDP forecast from 1.4% to a range of 1.6-1.8%, with the main positive factor being the 400 billion baht economic stimulus package. If fully disbursed, this could boost GDP by up to 0.4 percentage points through two main channels: the "Thai Help Thai Plus" program (the first 200 billion baht), expected to stimulate private consumption, and energy transition investment measures (the latter 200 billion baht), which will drive public investment.

A key issue is that the latter 200 billion baht faces constitutional uncertainty, pending a ruling by the Constitutional Court on whether the borrowing decree complies with the constitution. If the court disallows it, the GDP upside will shrink accordingly. INVX assumes actual disbursement at only 55% of the total amount, not 100%.

In a world of persistent complex risks, high oil prices, rising bond yields, and the Fed signaling rate hikes, INVX recommends a “Selective Buy” strategy focusing on three themes.

The first theme is Earnings Play stocks expected to deliver strong profit growth in Q2 and the second half of 2023, both year-on-year and half-on-half, including ADVANC, AP, GULF, MINT, MTC, SCGP, and TIDLOR.

The second theme is Defensive stocks with high pricing power that can withstand rising costs and inflation, such as those in telecommunications, healthcare, and commerce sectors.

And the third theme is New Normal stocks positioned on the S-Curve and benefiting from the energy transition, including clean energy, industrial estates, and related businesses.

INVX wishes investors good luck.