It became a major surprise that drew close attention from the Thai stock market when the industrial giant Siam Cement Public Company Limited (SCC) announced its first-quarter 2026 results with an exceptionally strong performance beyond expectations.

The company reported a net profit of 6.223 billion baht, soaring 466% from the same period last year. Additionally, it announced a strategic partnership with PTTGC to study a joint venture in the olefins and polyolefins business in Thailand.

With its stock price having already risen over 24% since the beginning of the year, the question is how much further SCC's stock price can continue to climb this time?

SCC reported its first-quarter 2026 financial results, stating a net profit of 6.223 billion baht, an increase of 466% compared to the same period last year, marking a significant turnaround from the net loss recorded in Q4 2025.

The main supporting factor was a large stock gain from SCG Chemicals (SCGC), which indirectly benefited from the geopolitical tensions in the Middle East.

The conflict and supply disruptions in the Middle East acted as a double-edged sword that positively impacted SCC. These events caused transportation and distribution constraints for major producers in the region, leading to higher global petrochemical product prices.

Meanwhile, SCC managed its supply chain more effectively, gaining from wider price spreads and stock gains, resulting in petrochemical business profits exceeding most analysts' forecasts.

Besides the chemicals business, the core business of "SCG Cement and Green Solutions" was another key driver. This quarter, the company successfully raised cement prices while efficiently managing production costs.

Focusing on eco-friendly products such as low-carbon cement also received positive market response, helping margins improve noticeably despite uncertainties in energy costs.

Regarding cash flow and financial position, reported EBITDA in this quarter reached 17.499 billion baht, while adjusted cash EBITDA stood at 14.929 billion baht, reflecting strong real cash profitability and liquidity management.

Another point to watch is the case where PTT Global Chemical Public Company Limited (PTTGC) and SCG Chemicals Public Company Limited (SCGC) signed a memorandum of understanding on 29 April 2026 to study the feasibility of a strategic joint venture in the olefins and polyolefins business in Thailand.

This collaboration aims primarily to strengthen supply chain security and enhance global competitiveness, focusing on developing high-value-added products to meet market demands.

The joint venture study, which depends on due diligence and approvals from both companies' boards and relevant regulators, is expected to show clear progress in the third quarter of 2026.

Analysts at Krungsri Securities Company Limited have a positive outlook on these results, noting that the net profit of 6.223 billion baht exceeded their research team's forecast by 24%.

This recovery, both from the previous year and the prior quarter, occurred across all business segments, led by the cement business restructuring that significantly reduced expenses and the petrochemical business benefiting unexpectedly from international situations.

The analysts believe the positive factors from Q1 will continue into the second quarter of 2026, expecting profits to keep recovering due to stable high demand in the cement and petrochemical sectors.

They also highlight the upside potential to watch—the partnership with PTTGC, which is currently in the feasibility study phase for the olefins and polyolefins joint venture, with clear progress expected by Q3 this year.

For strategic recommendations, they maintain a "buy" rating on SCC shares with a 2026 target price of 245 baht per share (currently under review for adjustments after the analyst meeting).

The main rationale is that SCC is one of the players set to benefit most from the "petrochemical industry recovery cycle" in the long term, which is just beginning to turn around.

However, investors need to monitor the sustainability of profit levels, especially if the Middle East situation eases or energy prices become highly volatile again.

Analysts view that SCC's ongoing business restructuring toward a "Green Business" model and continuous expense reduction will serve as important buffers, enabling SCC to maintain more stable profits than in the past.

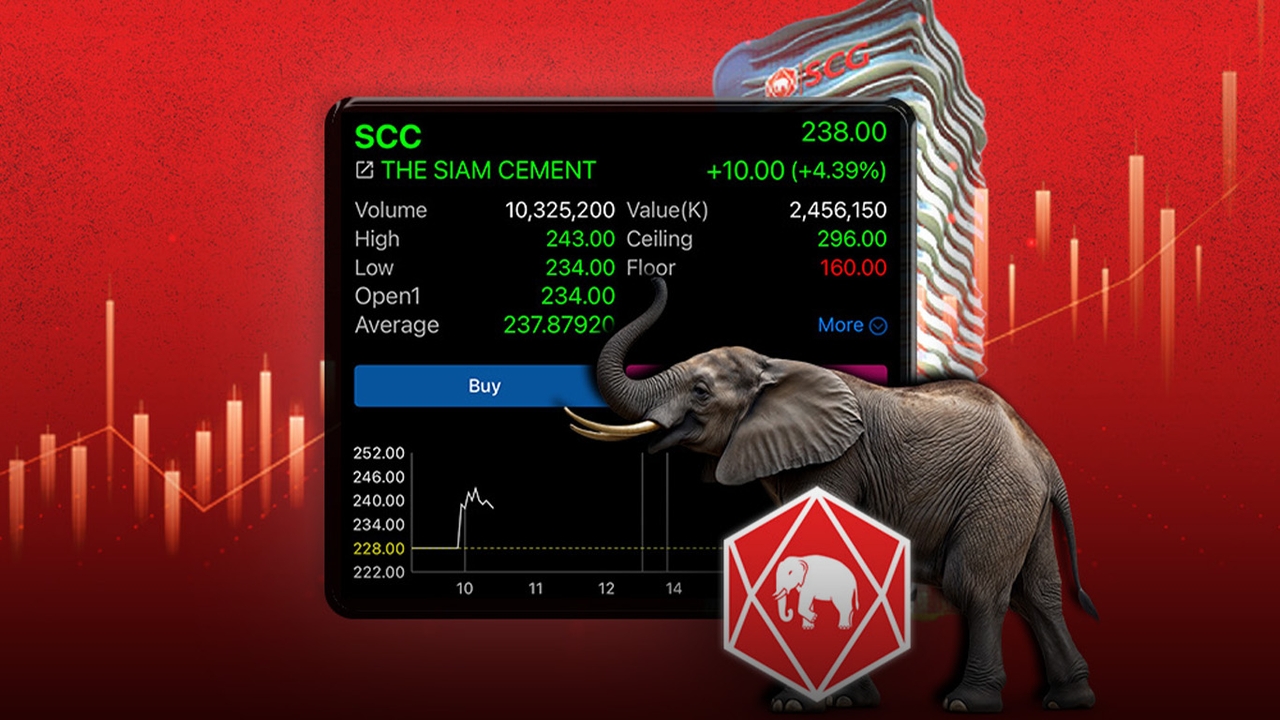

In 2026, SCC's stock is among the outperformers in the SET50 group, having risen over 24.25% since the start of the year, reaching 228 baht (as of the closing price on 29 April 2026), reflecting renewed investor confidence.

At the market open this morning (30 April 2026), SCC shares continued to rise. At 10:26 a.m., the stock price was 238 baht, up 10 baht or +4.39%.

According to data from the Investment Analysts Association (IAA Consensus), the average target price set by various analysts ranges from 245 to 260 baht, indicating that based on the current price, SCC shares still have approximately 5-10% upside potential.

In terms of valuation, SCC currently trades at a price-to-earnings (P/E) ratio of about 19 times, alongside a dividend yield ranging from 2.72% to 3.57% annually.

For stock market and investment news, visit Thairath Money at

Follow the Facebook page Thairath Money at this link