Recently, the Bank of Thailand (BOT) has been conducting a public hearing from 7 May to 5 June 2026 on a draft proposal to temporarily relax the Loan-to-Value (LTV) regulations and related housing loan rules for financial institutions and specialized financial institutions for another year.

In simple terms, the BOT is considering whether to "extend" the measure allowing 100% loans for houses and condos until 30 June 2027.

Although this has not yet been officially enacted, most real estate market participants and operators believe the measure is likely to be extended because Thailand's property market remains fragile, with large unsold stock of houses and condos, high rejection rates of loan applicants, and consumer purchasing power not yet fully recovered.

This article from Thairath Money aims to clearly explain what the "LTV relaxation measure" is, and if this draft passes, how it will help those buying homes, condos, or even property investors. The change is not just about "borrowing more" but mainly about reducing the upfront cash burden on the day of home purchase—a major barrier for many.

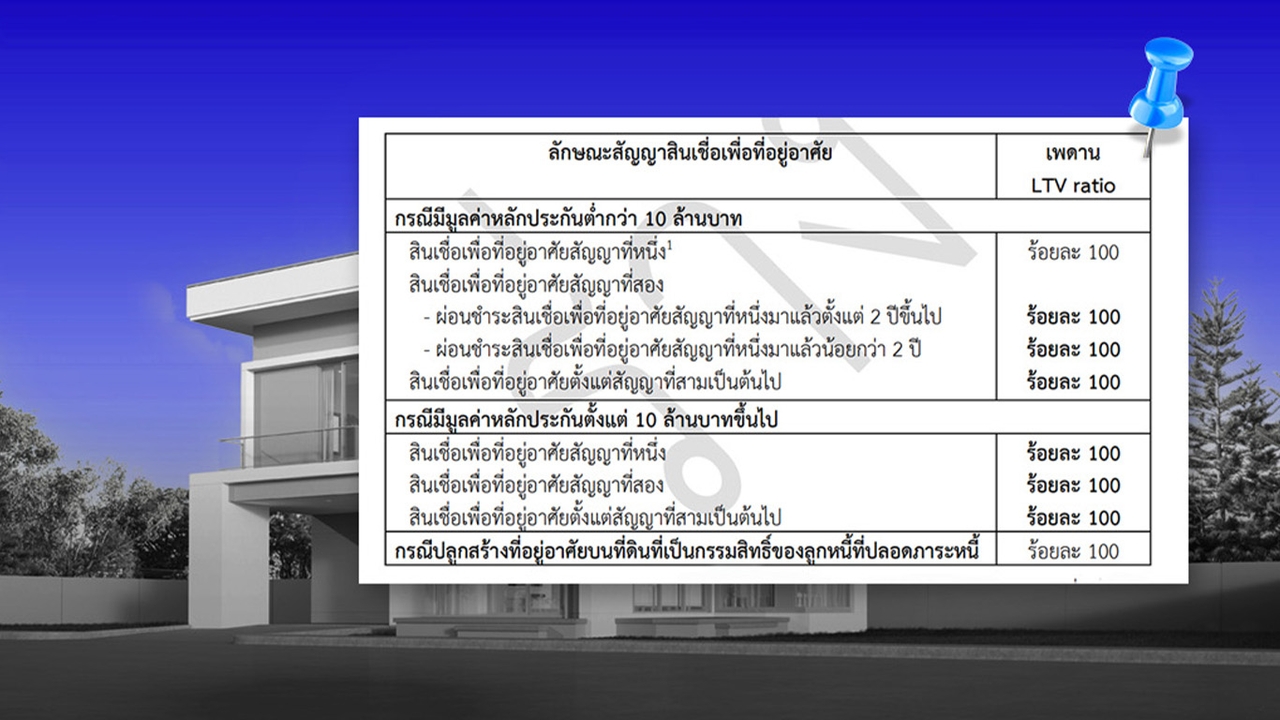

LTV stands for Loan to Value, which is the loan-to-collateral value ratio. Simply put, it is the guideline set by the BOT that determines "how much percentage of the house price banks are allowed to lend."

For example, a house priced at 3 million baht.

Previously, the BOT temporarily relaxed rules to allow 100% loans to support the real estate market and is now set to extend this again. If this draft is approved and effective from 1 July 2026 to 30 June 2027, nearly all homebuyers will still be able to borrow up to 100%.

1. First-time homebuyers

They benefit the most directly because if the relaxation expires, some might have to return to paying 10-20% down payments. But if extended, homes priced under 10 million baht can still be financed at 100%, reducing the upfront transfer payment burden, especially for young buyers who can afford monthly installments but lack large savings.

2. Second-home buyers

This group also clearly benefits. Under the new draft, even if the first home loan has not been paid off for two years, buyers can still get 100% financing for their second home.

This differs from the previous standard where many had to pay 10-20% down payments themselves. Beneficiaries include:

3. Investors or buyers of third homes and beyond

This is where the easing is most notable. Normally, this group faces strict controls as the BOT aims to curb speculation.

The new draft allows 100% loans even for the third property, helping to revive pent-up demand, especially in city condo markets and mid-to-high-end houses.

4. Homeowners building on their own land

If the land is debt-free, they can still get full 100% loans to build their house.

5. Buyers needing furniture or home renovations linked to their first home loan They can borrow an additional amount not exceeding 10% of the collateral value.

For example, for a 5 million baht home, they might borrow an additional 500,000 baht for renovations.

Because the BOT acknowledges that the real estate market is still slowing, with high unsold inventory and global economic pressures from geopolitics. Importantly, the BOT considers that speculative risks are still low because banks continue to apply strict lending criteria and financial conditions remain tight.

However, even with 100% loan availability, if income is insufficient, credit is poor, or debt burden is high, banks can still reject loan applications. Thus, this measure does not mean "easy loans" but rather reduces the upfront cash burden for those who can genuinely afford monthly payments. Although the rules allow borrowing the full amount, borrowers should remember "just because you can borrow the full amount doesn't mean you must." Financial institutions and specialized banks (such as GH Bank and Government Savings Bank) will still rigorously assess debt repayment ability under the principle of "Responsible Lending."

If this draft is approved, in the second half of 2026 we can expect:

Especially in city condos and mid-to-high-end detached houses, which have faced interest rate and loan difficulties over the past 1-2 years.

Source: Bank of Thailand

Follow the Facebook page: Thairath Money at this linkhttps://www.facebook.com/ThairathMoney